Is Will Hutton Actually Stupid Or Just Playing One On The Internet?

Is Will Hutton Actually Stupid Or Just Playing One On The Internet?

Or does he think we're stupid?

Will Hutton’s off on one of his usuals. We out here have no idea how our money should be invested or spent so it really should be handed over to the clever people like Will Hutton who will direct everything to their - sorry, our - benefit.

Really. Totally.

So, the claim this week is that the UK doesn’t invest enough:

His first advantage is that the economic evidence is unambiguous: the state does not “crowd out” investment, and low taxes do little to stimulate enterprise.

Both those claims are toss but let’s go a little further:

One important avenue to growth, cited in the Labour manifesto, is the prospect of unleashing some of the £1.4tn funds fossilised in Britain’s 5,100 defined benefit pension fund schemes. Linked to a generous fraction of workers’ final year’s pay, they have become a financial burden. To wind them up, companies have closed them to new members, creating a £1.4tn universe of wholly risk-averse zombie funds. They need to be consolidated into bigger funds that can take risks – and the money made to work to accelerate Britain’s investment recovery.

It’s precisely because those funds are closed to new entrants that near all of them are in run off. That is, they’re not investing money now that might be used to start paying a pension in 25 years’ time and might still be paying a pension in 50 years’ time. They’re paying out a pension right now. Now, there are fairly strict rules about this - most of which benefit “investing” in gilts because Chancellors can and do force such pension funds to fund government and Chancellors’ promises - but it’s also true that these funds aren’t getting any new money in but they have really a very good idea of what their expenditure is going to be and when. Bonds - not equities - are the right investment policy therefore.

Now, there might well be value in currently accruing pension funds being given a lot more investment freedom and that would increase stock market exposure. More likely to be foreign than UK but there we are. It’s possible to imagine that allowing funds in run off more equities in their funds would be a good idea for both funds and the market. But that’s not, not quite, what Willy is proposing. Rather, he wants all those lovely pensions savings to be “invested” the way he thinks they should be. The “invested” is because they’ll actually be spent, not invested. Spent on green and DEI and ESG and the rest.

But, you know, all too many people can’t see a pot of money without deciding they know how it should be spent best.

The real point here is this:

There is the tool to hand. One of the most startling policy successes of the past 20 years has been New Labour’s Pension Protection Fund (PPF), established in 2005, which takes over the management of distressed defined benefit pension funds, guaranteeing the future pensions. Managed with great professionalism, the PPF has already consolidated more than 1,100 pension funds and is currently worth £33bn with a £12bn investment surplus – one of the most successful funds of its type globally in securing high investment performance. Industry insiders believe that there is another £600bn locked up in small, high-cost zombie funds that could be liberated for productive investment.

The first staging post would be to scale up the current PPF to at least £100bn. Conservative objections that this would leave the pension funds with no fiscal backstop can be easily overcome; backed by the state, the PPF will become the new backstop via a guarantee that does not score as public borrowing.

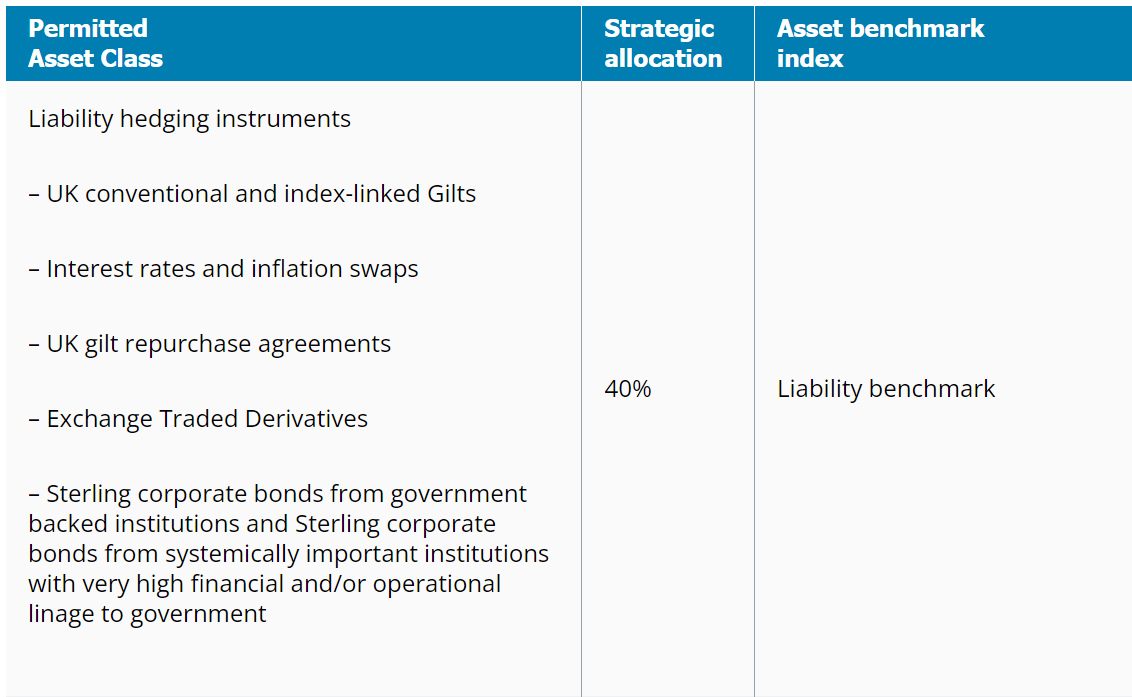

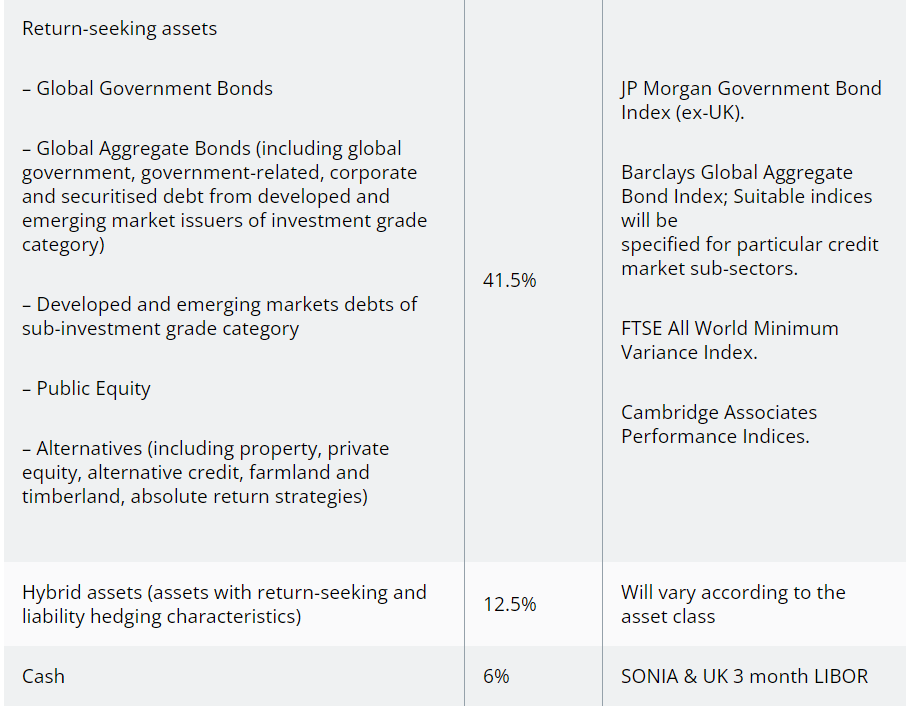

You just can’t leave money lying around without someone coming in to nick it, can you? But even that’s not the point. Here’s the PPF investment policy:

Our asset allocation is different from the allocations of average defined benefit pension schemes in the UK. This is because we need to be solvent at times when general pension schemes are significantly underfunded. We need a low risk strategy that aims to be relatively uncorrelated to the funding levels of the schemes we protect.

A little hint here. “Liquidity” in pensions means “not equities”. And here’s the actual portfolio allocation:

Will Hutton’s going to boost equity investment by taking over and adopting the investment philosophy of a pension fund that deliberately, with malice aforethought, pretty much doesn’t invest in equity.

Now do you understand why the general view is that either Willy’s an idiot or he’s doing damn well playing one on the internet?

Is that the "Will Hutton" who has managed to bankrupt just about every organisation he's had any executive authority over? If it is, then frankly I'd prefer to take investment advice from The Downing-Street Cat!

I think it makes more sense as a "nice pension fund you got there pity if anything regulatory would happen to it" type of shakedown,