MMT Once Again - Of Course Banks Don't Invent Money

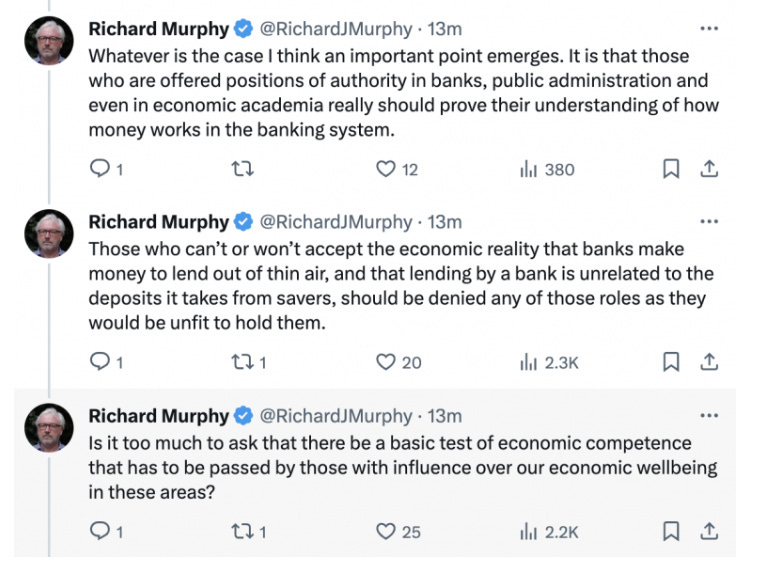

MMT Once Again - Of Course Banks Don't Invent Money

They lend out deposits, silly

As is so often true we can use reality to confound a presumption by Professor Richard J Murphy. It always coming as something of a surprise to him that reality does in fact exist.

So, there’s this from Lloyds Bank:

The net interest margin at Lloyds fell to 2.94 per cent in the first-half from 3.18 per cent a year ago,

The net interest margin for a bank is the difference between what it’s charging on loans out as opposed to what it’s paying on deposits in. It’s the one fundamental number in banking - this must be a positive gap because that’s where the money to do everything else comes from.

OK, so why has this margin fallen?

Higher rates drove a profits boom among banks last year. This is because lenders passed on rate rises more quickly to borrowers than to depositors, expanding their net interest margins. These margins, the difference between what a bank charges for loans and pays on deposits, are narrowing as savers have become more active at moving money to accounts that pay better rates of interest.

We, we depositors, have woken up a bit and decided that if our bank isn’t offering us much on our deposits then we’ll move around a bit to find someone who is.

Well, OK, bit of competition sharpens prices, nowt unusual about that really is there?

Except we’ve got to ask ourselves well, why is the bank paying anyone any interest? Banks just invent the money they lend therefore they don’t actually need deposits. So, what’s happening?

Now we’ve looked at this contention before and gone into proper detail about why it’s wrong (see again here).

This result from Lloyds is just an interesting little proof of it. Depositors are willing to move money out of Lloyds unless they get better interest. Therefore Lloyds has to pay better interest thereby lowering its profits. Because Lloyds really, really, needs those deposits. In fact, Lloyds goes bust without those deposits.

That is, banks do not just invent the money they lend. They must have deposits - therefore it’s useful to say that banks lend out consumer deposits. Because, by and large and at the end of the day that is exactly what banks do. They must attract deposits to fund their lending - therefore banks lend out deposits.

Modern Monetary Theory is quite right in saying that the presence of a deposit doesn’t determine the creation of a loan. But if banks are willing to lose profits in order to gain deposits then they really, really, do need deposits. For they fund lending.

I know you’re debating with a lunatic (Murphy, not me) but I really wish you weren’t *also* wrong in some annoyingly subtle ways.

In particular: you conflate two distinct steps in the process of 'taking' a deposit or 'making' a loan in your various writings on this topic. The result is that you confusingly use 'deposit' to mean both the cash/reserves that a customer hands over to a bank AND the liability that the bank subsequently records to that customer. But these are clearly two completely different things, not least because the former is an asset of the bank and the latter is a liability.

Similarly, you seem to use the word 'funding' to mean two different things too! Sometimes you use it to mean 'the actual cash/reserves needed to satisfy outflows' and sometimes you mean ‘the liability that matches any newly created asset on the balance sheet’. Again, one is an asset and the other is a liability. They can’t possibly be both at the same time!

Can I humbly suggest the following:

* When talking about cash or reserves that are in the possession of the bank you say just that: cash, a balance sheet asset.

* When talking about something the bank *owes* a customer, then call this a deposit. A _liability_ of the bank. But don’t use ‘deposit’ in other contexts.

They’re linked, of course: when a customer ‘makes a deposit of cash’, the asset side of the bank’s balance sheet increases (there’s more cash in the vault or reserves at the BoE), and the liability side also increases (a matching liability, the ‘deposit’, is recorded as an increased balance in the customer’s account). But they’re two different concepts.

This is important because it lets us tease apart the constituent parts of your go-to example of a bank making a loan to a customer, to see exactly where Murphy is wrong. We can break it down into 1) the creation of the loan, followed by 2) the (likely) withdrawal of the loan amount.

In part 1, the balance sheet is updated as follows:

* A new asset is created (the loan)

* A new liability is created (the deposit)

That deposit gives the customer the right to demand cash (or a transfer to another bank settled in central bank reserves) on demand. And so the bank needs to be ready to pony up the cash or reserves, but that hasn’t happened at the point the loan is made. It’s just something that could happen later.

This disentanglement is helpful because it means we can then distinguish between three different types of constraint a bank faces: leverage, liquidity and profitability which, collectively, lead to the empirical phenomenon that ‘deposits usually roughly equal loans’. But the key point is: this observation is not an iron law of economics or mathematics. It just works out like that in practice.

These are the constraints I think are in play:

1. The primary constraint on how many loans a bank can make is the degree of leverage it is allowed to have (or considers prudent). Specifically: how big can the asset side of the balance sheet be relative to the bank's equity? The answer to this is informed by thought-experiments such as ‘do we go bust if x% of our customers default and we have to write down the value of our loan book by y%?’ This is the main reason Murphy is so obviously wrong. There is a practical, and regulatory, limit on the prudent ratio of loans (or assets more generally) to equity. (Note: equity, not cash).

2. As a separate question, we can then ask: how much cash or cash-like stuff should a bank have on hand at any given time to satisfy anticipated cash outflows? This is a liquidity question. The bank needs to have a model for what proportion of its deposits will be demanded as cash on any given day, along with assessment of likely inflows and other non-deposit outflows.

3. And then there’s the question of profitability. Each asset on the bank’s balance sheet (loans, cash, whatever) is there because somebody agreed to let them create/buy that asset. What did the bank give them in return? A promise to pay interest? A promise to pay some fixed amount in the future? In any case, what is that corresponding promise worth? The answer to that is the liability that we say ‘funded’ the asset. And a key insight (which you make in your post) is that successful banks pay less for funding than is paid to them on the assets created/paid for by that funding. And deposits can be a cheap form of funding as no/little interest is paid. But they’re just one form of funding. In other words, deposit funding isn’t special because it brings cash in to the bank - there are lots of ways of bringing cash in to a bank. Deposit funding is special because the liability it creates is usually pretty *cheap*.

Now, it so happens that the amount of cash a bank tends to have on hand is roughly equivalent to the amount of deposits it holds. eg check out the balance sheets in the annual reports for pure-ish-play banks (eg nationwide or even Lloyds). But this is mostly an artefact of the interplay of the above… and not because of some iron law of nature that ‘deposits are needed to make loans’. Because that statement just ain’t true.

So now we can explain why banks can’t create deposits ad infinitum (and hence why Murphy is of course wrong).

* It’s imprudent to lever the bank too much. This is point 1 above.

* You do need to have some cash on hand in some proportion to the amount of deposits. And cash, like any other balance sheet asset, needs to be funded. And one of the cheapest forms of funding is deposits! (I know this seems a bit circular.) The point is: banks *could* fund the cash on their balance sheet some other way (eg a lot of repo perhaps). It’s just that they’ll likely make less money. This is the interplay of points 2 and 3.

Net-net: Murphy is wrong because (point 1) bank management teams are usually not insane and so don’t lever themselves up beyond a certain point (and prudential regulation exists in any case) and (points 2 and 3) retail deposits are cheap so basic profit-seeking encourages banks to attract as many as possible.

As I’ve said before, I applaud your efforts to fully expose the madness of Mr Murphy. But I can’t help thinking you’ll be more successful in this narrow area if you could just be a bit more precise with your language!!!