This *Is* A Surprise- Nick Shaxson Is Spouting Bollocks Again

This *Is* A Surprise- Nick Shaxson Is Spouting Bollocks Again

Yep, the bloke who wrote a book about tax dodging while living in Switzerland

Nick Shaxson is one of the dangerous ones. It’s not that he spouts bollocks for many manage to achieve that. It’s that he spouts bollocks that others believe then go and build upon. Saw just last week a video from Grace Blakeley about how The City is a “private corporation” and so can do whatever it likes. Almost certainly derived from Shakxon’s “Treasure Islands” book. Also hopelessly wrong. The confusion is simply that corporation is a very slightly archaic name for the city council. The “Corporation of Birmingham” is - or at least was - Birmingham city council. So too the “City Corporation”. It’s the local council for the City of London. OK, being British it’s got a bit of history attached, ranks as a county by some measures, still has the business (or if you prefer, guild) voting system. But it’s the local council and that’s really about it.

Here we’ve the start of the next bit of Shaxonism.

Nicholas Shaxson is co-founder of the Balanced Economy Project, an anti-monopoly NGO

Ah, OK, so they’ve found a donor or three and they get to issue silly reports on that cash for a bit. The value of this does depend upon the usefulness of the reports of course. And this introduction isn’t looking good, it really isn’t.

For example:

This monopolistic power hurts consumers too. According to research by the economists Jan Eeckhout and Jan de Loecker, average global markups – the prices companies charge for goods above the cost of producing them – have risen from around 21% above costs in 1980, to 61% today. So a pizza that may have cost you £12 if markets had been as un-concentrated as they were 45 years ago, may now cost £16. Think of the £4 difference as a private monopoly tax that nobody voted for. Here, monopoly power is the connecting thread linking supersize corporate profits with consumer pain, in a phenomenon dubbed “greedflation”.

Well, it would certainly be fun if profits had risen to 61%. They haven’t, of course they haven’t, but that’s what Shaxon’s trying to tell us. Note that “above the cost of producing them” which is just wrong.

In the paper that Shaxon himself links to we get a very different explanation:

In this paper, our main goal is to document the evolution of market power for the US economy since the 1950s. First, we analyze markups, the most common measure of whether firms are able to price their goods above marginal cost.

OK, it’s markup, not profit. OK, that’s useful to look at, certainly. But it’s not, not at all, “the cost of producing them”. As the paper goes on:

Markups alone do not tell the full story about market power. For example, markups may be high because overhead costs or fixed costs are high. In that case, the firm charges prices well above marginal costs in order to cover fixed costs.

Hmm, dunno, could be that there’s been a capital intensification? There are now higher fixed costs to producing anything - a Marxist would certainly insist that this is an historical inevitability. So, the margin on any one piece of production has to be higher in order to pay those fixed costs. But fixed costs are part of the cost of producing something.

While we do find that there is an increase in overhead costs, the rise of markups cannot exclusively be attributed to overhead. Markups have gone up more, and as a result, so has profitability. The increase in both markups and profitability provides evidence that market power has increased.

That’s the paper again, not Shaxson. That is, Shaxson is misreading - or misrepresenting - the very paper he himself calls into evidence. Tsk.

We can even take this further than either Shaxson or the paper does. From the paper again:

More important than the increase in the aggregate markup, the main insight is that the distribution of markups has changed: the median is constant, and the upper percentiles have gone up substantially. This rise in markups by a few firms has gone together with reallocation of economic activity. Few firm have high markups and are large, the majority firms see no increase in markups and lose market share.

The effect is very concentrated, it’s only the very tippy toppy firms this has happened to.

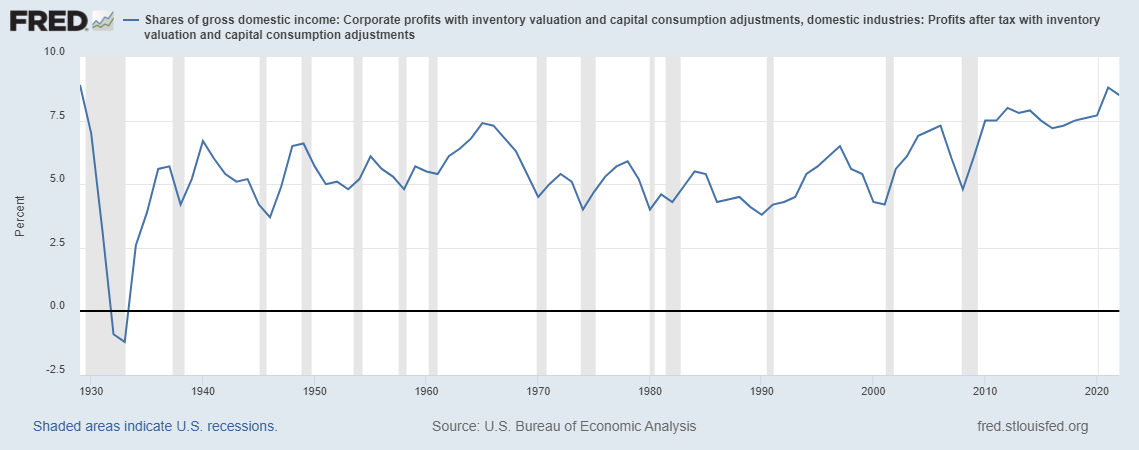

At which point, this:

That’s not - not quite - the right series but it’s still useful. Corporate profits as a share of GDP (before tax, inventory etc it’s more like 10% rising to 12% or so in the past decade etc).

OK, and now a detail of GDP accounting for the US. In these numbers the Bureau of Economic analysis includes all profits made by US companies within GDP. This is not correct. Profits made from the US economy are part of GDP. Profits accruing to US companies are part of GNP. The difference here becomes important. Because the global profits of the Big Tech companies are properly part of US GNP (accruing to US persons) and not part of US GDP (happening in America). But they do get included in the GDP numbers.

And what about those global numbers? MSFT made $165 billion last year. Google close to $100 billion. Facebook $50 billion -ish. Call it perhaps $300 billion - that’s 1 to 1.5% of total US GDP. And there we are, we’ve pretty much explained that increase in profitability concentrated as the paper says among the very few tippy toppy firms. And, as I say, those profits shouldn’t really be part of GDP even as they should of GNP.

But there we are, we’re done, we’ve explained what needed explanation. The big tech companies report their - vast, agreed - global profits in the US. These are, obviously, outsized as compared to the US economy and yes, they’re large enough to swing the whole economy numbers. Pfft, nothing else is required. It’s national accounting standards being imposed upon globalised businesses, little more than that.

But, you know, if you wanted to get to spend a few grants why not run with something that most grant makers aren’t even going to understand, let alone note.

But this has a knock on effect for the rest of the argument. Back to The Guardian:

When British farmers protested outside the Houses of Parliament earlier this year, they sent 49 scarecrows, after a survey had found that 49% of UK fruit and vegetable farmers said they expected to go bust within a year. The scarecrows stood in for real farmers, who are mostly too afraid to speak out. One farmer told campaigners they had grown 60 tonnes of salad potatoes for a large UK supermarket, only for the supermarket to suddenly cancel the order, leaving the farmer “financially screwed”. The arbitrary power that supermarkets wield instils fear, which the supermarkets leverage to impose take-it-or-leave-it fees and other unfair conditions on farmers.

The problem is our monopolised food system. Think of it as a vast profit machine shaped like an hourglass, with many food producers at the top, millions of consumers at the bottom, and a few dominant firms – such as giant supermarkets or global food traders – clustered at its narrowing neck, siphoning a cut from the passing traffic.

That’s something rather different but OK, let’s think about that. There are indeed many farmers and few supermarkets. It’s possible - possible - that the market power rests with the retailers and they then get to screw the price takers - price takers because there are so many of them - on the farming side. No no, this is a real thing to worry about, it could indeed be true.

So, is it true? Well, back around the turn of the millennium the British supermarkets had about the best net margins (ie, profits, not markups) of any national retailing market around the world. Tesco used to boast such nett of perhaps 6% of turnover. By the standards of the sector that’s big. Almost certainly reflecting market power too.

Then along came Aldi and Lidl. Their expansion has meant a sustained and substantial attack on British supermarket margins. Tesco now makes 2.5 to 3% of turnover. Around and about its cost of capital in fact. It’s very difficult to see anyone in the UK retail market making super profits at all in fact.

That is, the thing being claimed - excess market power leading to super-profits - probably was true of British supermarkets two decades back. Now it’s not true and the reason it’s not is the increase in competition. For which we’re all very grateful, of course. But it does mean that Shaxson’s both missed the boat and also is wrong. As there aren’t super-profits so and therefore there isn’t excess market power.

But that conclusion wouldn’t attract grants for researchers so therefore Shaxson is forced to write this sort of pish to get his project up off the ground.

Ho Hum, eh?

Even if it were true that some retailers were earning excessive margins, capitalism has an excellent remedy, which is that people like to make high returns on their capital and effort. Would Aldi and Lidl have come into the UK market a couple decades ago if Tesco's margins were low? Maybe eventually, but other markets would have been more attractive at the time.

Competition has indeed squeezed the margins of the supermarkets to eliminate any super profit.

However that still leaves the many small farmers as price takers, even when uneconomic, and probably more so that 20 years ago given the squeeze on retailers’ margins will inevitably increase the pressure to keep input costs down.

The answer must lie in the key words of your description: *many* farmers, *few* supermarkets. Food retailing has consolidated from thousands of small high street shops to huge supermarkets run by a handful of huge businesses; most farming remains small and fragmented, still in the world of the 1940s high street shop. Farming similarly needs to consolidate so that it can have price negotiations on equal terms with supermarkets, like the conversations that no doubt happen between Tesco and Unilever.