Yes, It's @RichardJMurphy Time Again

Aren't we the lucky ones

We’re warned that there must be - just must be - a ghastly stock exchange crash just about to happen. No, it’s obvious, innit?

Now, sure, it could happen. Might. Open to the idea at least. But I think I’d need rather better analysis than this:

You have been warned; markets are making no sense

This is the chart of the MSCI All-Country World Equity Index from Investing.com:

The index is a weighted measure of the change in equity shares around the world.

Why note this now? Simply because the index is, you will note, at an all-time high.

We are living in a world where nothing is working, where real markets are in disarray, and we face the risks of fascism in many countries, with some, from the USA onwards, already succumbing. Despite this, equity investing fund managers - probably using your pension fund - have pushed share valuation to this position.

I have three thoughts.

First, this makes no sense.

Second, this could only happen, in my opinion, because they are gambling with other people's (maybe yours) money, to extract a rental reward for themselves in the process.

Third, a crash is inevitable.

You have been warned.

Well, isn’t that the nefarity?

At which point, two points rather than the Solanum Tuberosum’s three.

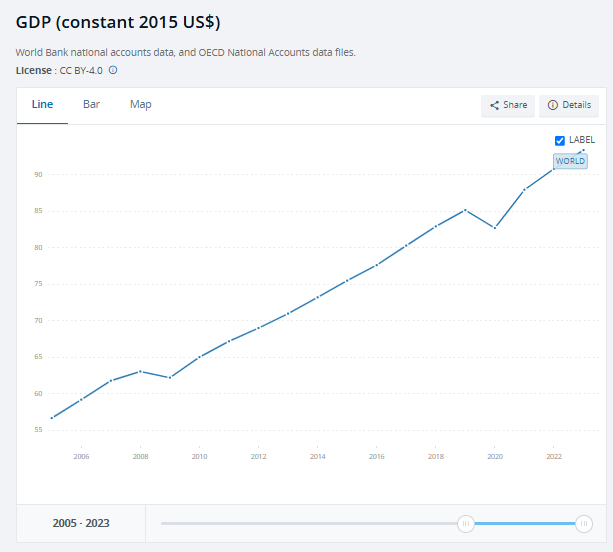

Stock indices are not inflation adjusted. Inflation in the US dollar has been some 60% or so since 2005. Other currencies perhaps more or less.

That is also not corrected for inflation (at the World Bank “current” means the $ of the year of measurement). We can look at the same data corrected for the varied inflation rates across the world:

So we’ve about a - you know, roughly - doubling of the real size of the global economy since 2005 (and note these numbers only go to 2023). And we’ve an inflation rate of some 60% or so in the major international reserve currency.

From which we’re supposed to conclude that a 200% rise in the global stock markets is obvious proof that pensions fund managers are stealing our money?

More water with it Emeritus Professor Murphy. More water with it. Or, possibly, try checking what the fuck you think you’re talking about?

Tattie's right you know. There isn't a fund that outperforms the market. The annual percentage management fee compounds. In many jurisdictions, funds are obliged to invest portions of the capital in low-yielding approved assets. Rachel From Accounts wants to force funds to invest in minus-yielding ESG assets as well.

In most jobs you can't salary-negotiate your way out of the compulsory company pension/provident scheme, and get the employer contribution paid directly to you. There is going to be a fund manager somewhere leeching away at your assets. Fund managers provide no positive value, only negative value. The only legal kind of fund should be an index fund, with management fees capped at one half of one per cent.

That there is a crash coming is a different contention. Even with nations of people living paycheck to paycheck, private savings whether voluntary or forced have to go somewhere. The volume of private savings keeps increasing, exponentially higher than inflation. Money just keeps on pouring into market assets, from bourses to property to private equity to crypto. Ergo the FTSE Dow and Nasdaq, housing prices, and look what's happening to Bitcoin. For that to reverse would take a huge economic collapse, where savers are forced to cash in. Fund managers may not like Trump's tariffs, but where the heck else are they going to put the money?

He’s a moron. Best ignored rather than amplified.

Monbiot has a platform via the Graun and some sort of reputation as a serious public intellectual so is worth your time challenging and debunking. Murphy? Not so much.